24 Feb How To List Business Personal Property

Why do I have to list property?

Property must be listed each year so that is can be valued (assessed) and taxed for property taxation.

- North Carolina Machinery Act provides the statutes governing the listing of property for property taxation.

In this book, we are going to deal with the listing of business personal property.

North Carolina Department of Revenue has a standard form that can make listing business personal property easier. This form can be downloaded from their website at: http://www.dor.state.nc.us/downloads/listingform_archive/2016/listingform.pdf

When do I file the listing form?

The listing period begins on January 2nd each year. The deadline for listings is January 31st. Completed forms must be postmarked by the U.S. Postal Service no later than January 31st to avoid a 10% late list penalty.

Who should list?

Anyone owning property located in a North Carolina county which meets the following criteria:

- Unlicensed automobiles, trucks, trailers, campers, motorcycles, and recreational vehicles.

- Mobile Homes, boats and motors, farm equipment and machinery.

- All improvements or changes to leased property.

- All business personal property.

How do I list?

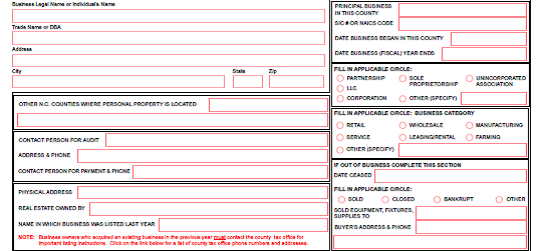

This is where the county listing form or state approved listing form is used. Please fill out all information on the top of the first page. If something does not apply to you, do not leave it blank, simply enter “N/A”.

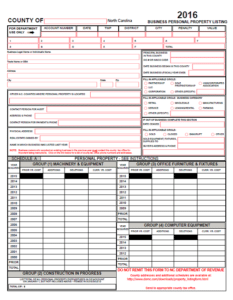

Schedule A

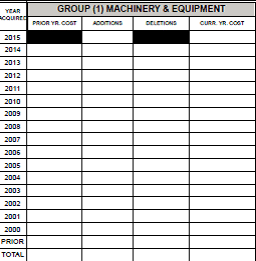

Personal property in the categories of Machinery & Equipment, Furniture & Fixtures, Computer Equipment, Leasehold Improvements, Expensed Items, Construction in Progress, and Supplies should be reported in this section. Fully depreciated assets should also be included.

Capitalized assets are property items that are expected to have a useful life of more than one year and are listed in the Machinery & Equipment, Furniture & Fixtures, Computer Equipment, and Leasehold Improvement groups. Examples of these types of Business Personal Property are:

- Office Equipment

- Office Decorations

- Desktop Computers

- Printers

- Maintenance Equipment

- Operating Equipment

- Office Furniture

- Point of Sale Equipment

Supplies and Expensed Items are also a types of property that is to be listed. These cost are expensed on your financial records but should still be listed for business personal property. Examples of these types of business personal property are:

- Fuels

- Spare parts

- Office Supplies

- Operating Expense

- Small Tools

- Items used in the process of providing a service

Construction in Progress is the cost you have spent for personal property items still under construction on January 1 but have not been placed into service. This amount represents the investment you have made in this property and is to be listed.

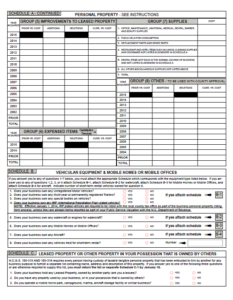

Schedule B

This section is for Unregistered Motor Vehicles, Multi-year or permanently registered Trailers, Special Bodies on Vehicles, International Registration Plan plated Vehicles. Include the Year, Make, and VIN number of the vehicle, as well as, the cost and year purchased.

This section also includes:

- Watercrafts and Engines

- Mobile Homes or Mobile Offices

- Aircraft

- Vehicles held for short-term rental

Schedule C: Leased Equipment

Property that is in your possession, but owned by others should be listed in this section. This includes any personal property which is loaned, leased, or otherwise held and not owned by you. A complete description and ownership of the property should also be reported in this section:

- Operating Leases either have no ownership transfer or a significant buyout clause at the end of the lease. These leases do not generally transfer ownership at the end of the lease term. These are not financial arrangements. The person in possession of these items are not responsible for the property taxes. The leasing company should report this property to the county.

- Capital Leases are considered to be a financial agreement (loan) and are reportable by the taxpayer in Schedule A. These leases have little or no buyout amount at the end of the lease. Assets purchased under a capital lease are usually capitalized on the financial records of the taxpayer and considered to be their property.

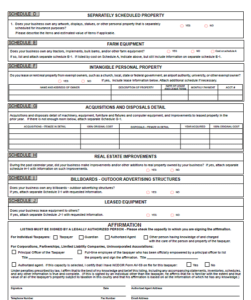

Schedule D-J

- Special Property

- Farm Equipment

- Leased or Rented Property from exempt owners (church, government, schools, etc.)

- Detail of acquired and disposed assets

- Real Estate Improvements

- Billboards

- Leased Equipment

Now that you have gone through your list of assets and determined where each item is to be listed, let’s look at how to put the information on the form. Each group or category has a box. In the first column of each box is a date starting with the most current year and descending in order until you reach “prior”. Items to be reported in each group should be summarized by year of acquisition and cost.

- Historical cost should be listed in the original cost column corresponding to the proper year acquired. Historical cost is amount paid for the item when it was new, along with all cost associated with placing the item into operations. If a taxpayer buys a business that is already in operations, the cost of the equipment when it was new should be used, as well as the original in service date of acquisition, not the purchase price of the used property.

- Any additions or deletions during this year should be listed in the corresponding additions/deletions column. The current year cost should then be calculated and recorded in the current year cost column by adding/subtracting the additions/deletions from the original cost. Each column should then be totaled.

Listing Form Example

Why is it Important to List?

If all property in a county were correctly listed, appraised, and taxed, the tax rate could be significantly lower.

Therefore…

- It is essential that every tax program be fair and equitable.

- It is essential that correct information be used in every listing.

- Historical cost needs to be provided as it is the basis for consistently appraising personal property.

- A review of the taxpayer’s records is essential in order for everyone’s property to be valued correctly.

Sorry, the comment form is closed at this time.